Do you know that itch to buy some stocks? Well, I am feeling it now… It’s been quite a while since I purchased anything new due to various expenses and I think I am going to pull the trigger soon.

Since I am an IT engineer I figured that it would make sense to have some exposure to tech sector. I am trying to figure out which tech stock to choose at the moment to be added to my portfolio.

I am interested in the following characteristics when choosing my stocks:

- Dividend yield

- Payout ratio

- P/E ratio

- Dividend increase rate

- Years increasing dividends

- Debt level (Quick ratio and Total debt to equity)

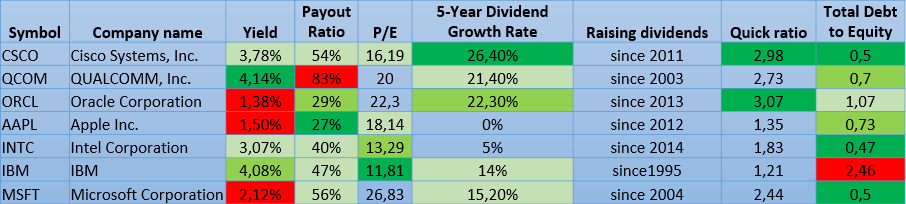

I came upon a post from DivHut who is trying to decide which tech stocks to invest to. I thought his list of possible stocks would be a good starting point for my own analysis. Based on criteria I am interested in, I evaluated each of the company:

One of the most important things for me as dividend investor is the annual yield of dividends. I would like it to be at least 2.5%. As we can see from the above table, only 4 companies from the selected list suit this criteria (CSCO, QCOM, INTC & IBM). I also prefer if company’s payout ratio does not exceed 60%. If it’s higher than that, there is bigger risk that company will not grow its dividend or even cut it in the near future. This reduces the list by one more company – QCOM’s payout ratio is whopping 83% which looks too much to me. This leaves me with 3 companies to consider – CSCO, INTC & IBM.

Price/Equity ratio looks best for IBM. INTC (with P/E of 13.29) and CSCO (P/E 16.19) have higher P/E ratio but are also undervalued at the moment in my opinion as their P/E is lower than industry’s.

Recent dividend growth rate is bigger for Cisco and I would expect it to raise substantially for at least the next few years. What I like about IBM is the fact that it’s raising dividends for more than 20 years in a row and the payout ratio is not that high. INTC is lagging behind with the lowest growth rate of these 3 companies. At this point I would cross this company out and stay with considering CSCO and IBM.

Cisco’s financial stability is looking much better than IBM’s. Quick ratio is a measure of how well a company can meet its short-term financial liabilities. It can be calculated as follows: (Cash + Marketable Securities + Accounts Receivable) / Current Liabilities. The bigger the ratio, the better situation of the company is to pay their short-term debts. CSCO (current ratio 2.98) looks much better than IBM (current ratio 1.21). Total Debt to Equity ratio is the worst for IBM – this is another signal that the financial situation of this company is looking worse than the one of competitors. Cisco is looking financially healthier.

Prices of both IBM and CSCO recently fell mainly due to falling revenues. I believe that the reaction of markets was too big and they can still turn around. Also, their dividend is still safe due to low payout ratio. Price fall is a good opportunity to enter the market. From my previous experience it works out in most of the cases. Even if the price stays at these levels, dividend yield should still earn something.

Looking at the above table, overall stats are looking best for IBM with CSCO trailing behind a little bit. However, I would still prefer CSCO due to my personal experience and exposure to IT in my workplace. The bank I am working in is using Cisco’s software – VPN client AnyConnect (for remote working), Webex (for conferences). It was used in my previous company as well. IBM software is also used but usually it’s used by smaller field of people and is not that critical. Even bigger factor is the network solutions Cisco provide – I can often see Cisco boxes arriving to our office. When you speak about network, you often speak about Cisco. What I like about Cisco is that they have moat in their industry – Computer Communications Equipment. Most of other companies I was able to find in this specific field are at least 10 times smaller than Cisco. Of course, small size may be an advantage in the long run but it’s hard to predict which of them will be successful. Also, they will not be paying dividends before they reach some sort of maturity in their business. After discussion with my colleagues at work, we also came to a conclusion that Cisco is not going anywhere – there are too many companies depending on their network solutions. On the other hand, IBM has more risks as they are operating in more fields than Cisco. E.g. Amazon Web Services are putting a lot of pressure on server-focused companies like IBM. Recent selling off of IBM stocks by Warren Buffett also shows signs that the company is not doing that well.

So I will put some more thought into Cisco, consider potential risks and decide if it is worth investing to.

Do you have any tech companies in your portfolios? Would you choose another one from the list or stay away from tech sector altogether?

Thanks for reading!

I am long:

– CSCO

– QCOMM

– INTC

And I’m active looking at IBM to add them to my portfolio. Thanks for the write-up of your analysis, good stuff!

Nice choice! 4 companies that passed my initial check for yield.

I think IBM is similar to Cisco at their current price. It’s more of a personal preference to value CSCO better than IBM.

Great assesment of those tech companies. Got 4 of them: CSCO, MSFT, IBM and QCOM. My entry point on IBM was a little high at about $180 per share (ouch!), but I’m comfortable keeping them. Still produces some nice juice dividends :).

SD –

Wow, you’ve got a lot of exposure to tech sector. What percentage of your portfolio does it have approximately?

All 4 of your companies have moat in their respective industry so I think it’s good choice! And industry leaders are often a little bit overrated so I wouldn’t worry too much about your entry point in IBM. We’re here for the long haul!

-BI

It’s like I’m reading DivHut’s post from earlier this week again lol jk. Same stock picks, same order. Nice to see another IT person in the DGI community. I am the same and like going off of the products or services I use on a regular day basis. I feel like out of those choices, CSCO pulls ahead. They were also the first dividend stock I ever owned, so maybe I have a soft spot for them, who knows. But they have been doing very well in my portfolio and have also been gaining a lot of attention by other members of the DGI community as well.

Hi DD,

Thanks for the comment and you’ve got good eye and memory!

Actually, the list IS from Divhut’s post (added a link to his article for courtesy). I was thinking about evaluating tech stocks for a while and his article’s list was a good starting point to apply my own analysis 🙂

CSCO also looks best for me for personal reasons in part but let’s give them credit for technical ratios as well.

Nice to see that you are also an IT person. What’s your field? I am a packaging engineer, dealing with mass distribution of software as well 🙂

I really appreciate all the comments and thoughts everyone has put into both posts here and on DivHut. The tech space would definitely be a first for me in my portfolio and I’d say that I’m leaning towards three names, MSFT, CSCO and last QCOM. While MSFT is not cheap these days, it still is showing a lot of growth with Azure and though a distant second to AWS from AMZN I think it can still make a lot more inroads in the cloud world.

Hi DivHut,

Thanks for stopping by! I fully agree with you, all 3 of them have moats in their fields and I still see potential. Looking at the financials, IBM also looks good but somehow they are not appealing to me – I can see too many risks in their business.

P.S. I hope you don’t mind that I borrowed your list for my analysis!

– BI

All good 🙂 I appreciate reading all the comments about the tech space. Thanks for reading DivHut too!

It is amazing to me how rare it is that a tech firm pays a dividend. If you liked the other metrics would you consider reducing the first dividend yield metric? If MSFT hit everything else is it that big of a deal that it is a .34 off on yield?

Hi Evan,

Thanks for stopping by!

In general I like MSFT because it is a leader in a few fields. I use MSFT products in my work everyday as do my 30k colleagues in the company I work in 🙂 However, I think it’s a little bit overvalued at the moment for my liking. The P/E is too high in my opinion. If the price went down, the yield would automatically come up if the payout stays the same or grows. Only then I would consider adding it to my portfolio. For now, other companies beat it at current valuation.

-BI